TOG reports full financials, -on Valentines Day.

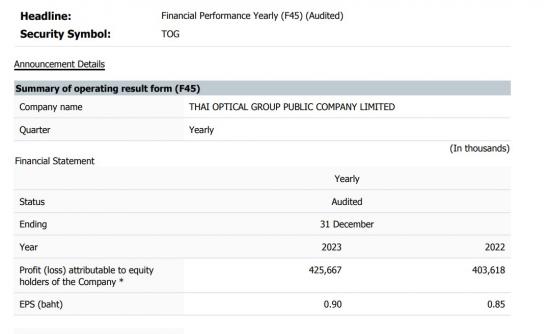

TOG (12.10) just after 5 PM yesterday reported its yearly financial statements to the SET. (Feb. 14th 2023)

Its a good to great report but needs more to say/analyze then first meets the eye. So here I do it, for us: Net profit for all of 2023 was 425.667 mill. Baht vs. 403.618, for year 2022. EPS came in at 0.90 Baht vs. 0.85 Baht, for year 2022, yes both at a record. TOG also, an hour later, announced a 0.45 Baht dividend per share, vs. 0.43 the year before, which is a 5% increase. Ex-dividend date is 12-Apr-2024 and Payment date is 02-May-2024. Remember, TOG pays dividends twice a year, with an interim smaller additional dividend, announced every early to mid August.

TOG's revenues for the 4th Q '23 was 860 mill. a a record, and nicely 20% above 720 mill. its average revenues per Q,, for the previous first 3 Quarters of last year Total revenues for all of year 2023 was 3.015 Bill. Baht, vs 2.96 Bill., for calender year 2022.

Net profits for 4Q. '23 was less, or 89.72 mill., (vs. 106.33 mill for 3 Q 2023), but this was due to: 1) far higher finance costs now and 2) less FX one time gains vs. the year before (3 mill. vs. 20 mill in 2022). Finance cost were 25.8 mill. vs 7.8 mill. the year before. Finance/interest costs have been increasing only of late, due to TOG new investments in higher margin Fx lenses, which will benefit revenues/profits most starting this year 2024! As here explained before in previous articles.

So if you add 17.9 mill (the net increase in finance cost) and + 17 mill. (i.e less in Fx gains) one can see 34.9 mill Baht difference

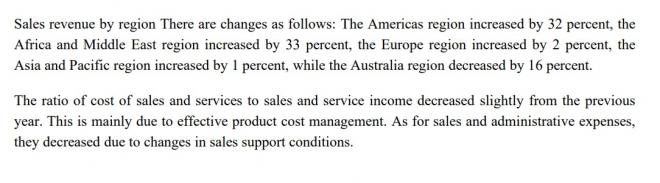

it would have brought net profit to 460 mill., or to just about 1 Baht per share! (0.97 EPS to be precise.) I also noted S & A cost dropped from 80.2 mill. to 67.6 mill. in 2023, due to better cost management on that! You can see some tables below and its text where growth came from, from their SET release yesterday Feb 14th 2023. BTW, TOG earned 132 mill. Baht in year 2019, just before Covit hit.

it would have brought net profit to 460 mill., or to just about 1 Baht per share! (0.97 EPS to be precise.) I also noted S & A cost dropped from 80.2 mill. to 67.6 mill. in 2023, due to better cost management on that! You can see some tables below and its text where growth came from, from their SET release yesterday Feb 14th 2023. BTW, TOG earned 132 mill. Baht in year 2019, just before Covit hit.

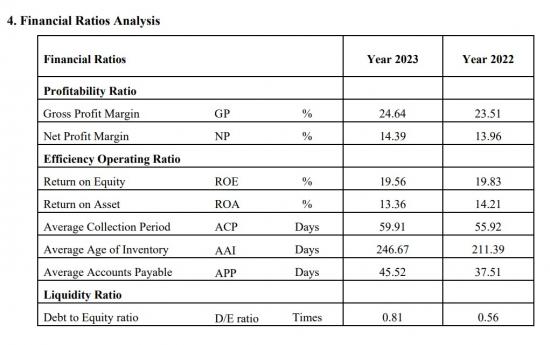

Duly note how both gross and net profit margins remain very solid, yet again. As is ROE, now approaching 20%. As is its ROA now at 14.21%, vs. 13.36% for 2022. This despite the increase of interest expense of late. (Tables & text below as taken from TOG's SET release yesterday). BTW, as of end of September: "Property, plant and equipment" was shown at 1,574,978 vs. the previous Q., was only 1,010,510. We see TOG is on a meaningful increase in capacity for this year 2024, due to strong global demand of its Rx, lenses.

TOG's p/e is barely 13 and its dividend yield on the current stock price likely right around 6%. Very undemanding for a leading export company which benefits from triple demographics and any potential further Baht currency weakness. Especially so compared to a lethargic on going SET bear market, which despite its sell-off still trades at a 30% higher p/e and 40% lower stated dividend yield, as compared to TOG which has strong growth in earnings/revenues prospects for this year and next, due to its strong global demand now supported by new rather large investments in higher margin Rx lenses. Buy view on TOG is so maintained!

Paul A. Renaud. www.thaistocks.com